What's next for the 'Big 3' Carriers

In 2019 FedEx cut Amazon as a customer. It was a smart move at the time. Amazon was showing signs that it had ambitions in logistics, and it was starting to take deliveries in-house while using FedEx for coverage of less profitable deliveries.

FedEx was confident. The late Fred Smith stated on television that Amazon could not easily replicate the infrastructure and processes that FedEx had built up over 40 years.

Fast forward to 2025. Amazon has become the largest retailer in the world. Amazon Shipping, its gig-model parcel carrier service, delivers an estimated 64% of Amazon’s shipments as well as shipments for major companies like Shipbob.

The uncomfortable truth FedEx faces today is that Amazon has become a shipping company faster than FedEx has become something else. And that “something else” is precisely the problem. After years of experimentation, it’s no longer clear whether companies like FedEx, UPS, and DHL, have a growth strategy that can compensate for the systemic loss of their core parcel delivery business.

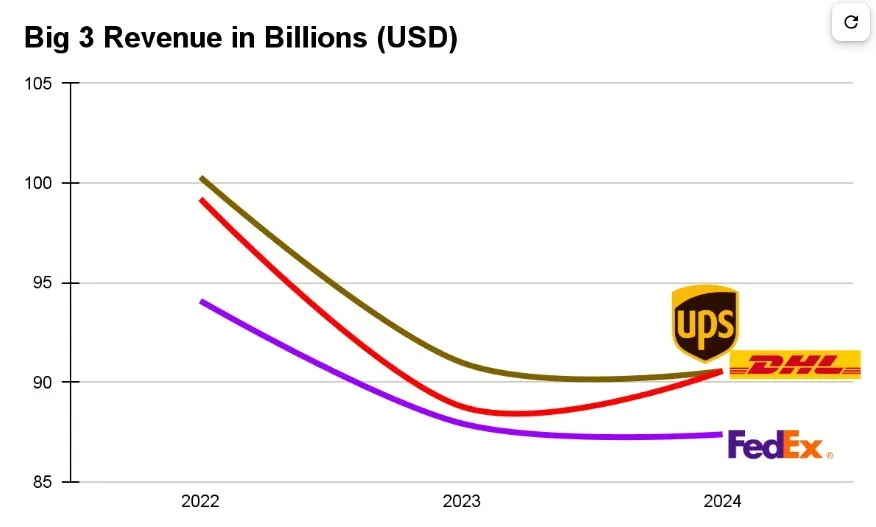

The Big 3 - FedEx, UPS, & DHL

FedEx is not alone in it’s struggle. UPS and DHL are in the same boat. I refer to them as the Big 3 because they are the only true global parcel delivery companies, and they coincidentally have very similar revenues.

- DHL Group $95B

- UPS $91B

- FedEx $87B

To the largest retailers and shippers in the world, the Big 3 are their most important parcel carriers — which is why it pains me to consider that they might possibly be in existential trouble.

Despite their scale, all 3 companies have had tremendous challenges growing their businesses. Sadly, their revenues aren’t even keeping pace with the average growth of Ecommerce, indicating loss of market share.

Read more:

{kind=link}

{kind=link}